Every project runs on a budget, and how well that budget is managed often determines whether the project succeeds or falls apart. Yet there are many organizations where costs spiral not because of big mistakes but because of small, untracked, or missed estimates, and suddenly the project is over budget with no clear explanation.

This is exactly where project cost management makes the difference.

Project cost management is the process of planning, estimating, budgeting, and controlling costs at every stage of a project so that it gets delivered without financial surprises.

In this guide, we will cover everything you need to know about project cost management, what it is, why it matters, the common challenges, best tools and software for project cost management, etc.

- 1.Cost management is a continuous process that spans planning, estimating, budgeting, and controlling costs across the entire project lifecycle, not something done once at the start.

- 2.Setting aside a few percent of the budget as a contingency reserve gives the project a financial buffer to absorb unplanned costs without derailing the baseline.

- 3.Reviewing costs weekly rather than only at milestones helps project managers catch variances early, while they are still small and manageable.

- 4.Scope creep is one of the leading causes of budget overruns, so a formal change process should evaluate the financial impact of every new request before it moves forward.

- 5.Cost is directly tied to the triple constraint, since scope, time, and cost are interdependent and a shift in one will almost always affect the other two.

- 6.Using tools that connect task tracking with budget data in one place makes it easier to spot financial risks in real time instead of discovering them after the fact.

What is cost management?

Project cost management is the process of estimating, budgeting, and controlling expenses throughout a project’s lifecycle.

It ensures a project is delivered within its approved financial baseline and remains profitable by preventing budget overruns.

Why is project cost management important?

Project cost management is important because it gives project managers the structure and tools to plan, monitor, and control spending throughout the project lifecycle.

Without it, projects run over budget, drain resources, and fail to deliver value, regardless of how strong the team or timeline is.

It turns financial visibility into a strategic advantage, helping organizations complete projects on budget while maintaining quality and stakeholder confidence.

Here we are pinpointing a few major points it enables:

1. Ensures financial control: Establishes spending boundaries and enforces discipline across all project phases. This ensures that every dollar spent is justified and aligned with project objectives.

2. Prevents budget overruns: Identifies potential cost risks early and puts corrective measures in place before overspending occurs. This protects the project from financial surprises that can stall or derail delivery.

3. Supports better decision-making: Gives project managers accurate, real-time cost data to make informed choices about resource allocation, scope changes, and trade-offs. When decisions are backed by financial clarity, they are more defensible and strategically sound.

4. Improves resource utilization: Ensures that people, tools, and materials are assigned efficiently without over-allocating or wasting capacity. This maximizes output per unit (currency) spent and reduces idle time across the project.

5. Enables accurate forecasting: Uses historical data and current performance metrics to project future costs with greater precision. This allows teams to anticipate funding needs and avoid last-minute budget requests.

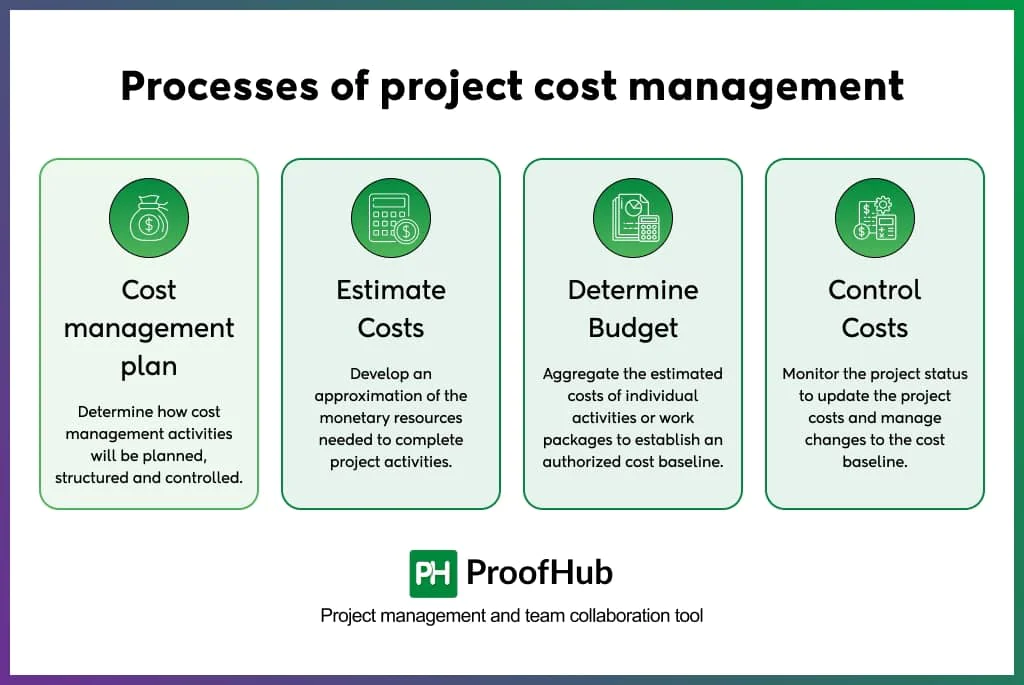

What are the processes of project cost management?

The four processes of project cost management are cost management plan, estimating costs, determining a budget, and controlling costs.

Each process builds upon the previous one, ensuring financial discipline from initiation through project closure.

These processes are:

1. Cost management plan

Sets the framework and rules for how costs will be managed across the entire project. The cost management plan defines the methods, tools, and procedures the team will use to estimate, budget, and control costs.

It acts as the financial governance document for the project, establishing standards for reporting, thresholds for variance, and the level of precision required in cost estimates.

Without this plan, cost-related decisions lack consistency and accountability.

2. Estimate costs

Determines the approximate financial resources needed to complete each project activity. This process involves analyzing work requirements and assigning a monetary value to every task, resource, and material involved.

Project managers use techniques like analogous estimating, parametric estimating, and bottom-up estimating to develop figures that are as accurate as the available data allows.

Strong cost estimates reduce the risk of budget shortfalls and set realistic expectations for stakeholders from the start.

3. Determine budget

Aggregates individual cost estimates into an authorized total budget and establishes the cost baseline. Once costs are estimated at the activity level, this process consolidates them into a unified project budget.

The result is a cost baseline — a time-phased spending plan that serves as the official benchmark against which actual costs are measured throughout the project.

It accounts for contingency reserves and aligns financial resources with the project schedule.

4. Control costs

Monitors actual spending against the budget and manages changes to the cost baseline. This is the ongoing process of tracking what is being spent, identifying variances, and taking corrective action when costs deviate from the plan.

Use tools like Earned Value Management (EVM) to measure cost performance, forecast final costs, and prevent unauthorized scope or budget changes from slipping through

Effective cost control is what keeps a project financially on track from kickoff to closeout.

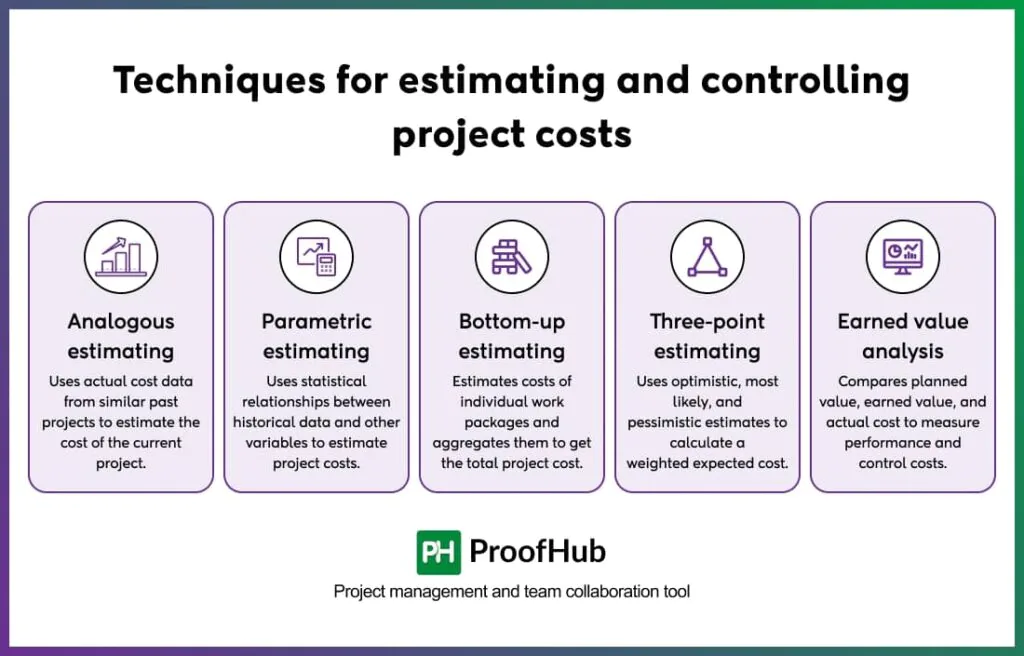

What are the techniques for estimating and controlling project costs?

The techniques for estimating and controlling project costs are Analogous Estimating, Parametric Estimating, Bottom-Up Estimating, Three-Point Estimating, and Earned Value Analysis.

These are the structured methods used by project managers to forecast expenses accurately and monitor financial performance throughout the project lifecycle.

Let’s read more about these techniques here:

1. Analogous estimating

The analogous estimation uses historical data from similar past projects to estimate current project costs.

It is a quick, high-level technique best suited for early project phases when detailed information is limited.

2. Parametric estimating

Parametric estimating uses statistical relationships between historical data and project variables (e.g., cost per unit, cost per hour) to calculate estimates.

It is more accurate than analogous estimating when reliable data and a defined scope are available.

3. Bottom-up estimating

Bottom-up estimating involves estimating costs at the individual work package or activity level and rolling them up to determine the total project cost.

It is the most accurate estimating technique but requires significant time and detailed project information.

4. Three-point estimating

The three-point estimating uses three scenarios: optimistic (O), most likely (M), and pessimistic (P), to calculate a weighted average cost estimate.

It accounts for uncertainty and risk, making estimates more realistic than single-point figures.

5. Earned value analysis

Earned value analysis (EVA) is a performance measurement technique that integrates scope, schedule, and cost data to assess project health.

It uses key metrics like CPI (Cost Performance Index) and SPI (Schedule Performance Index) to detect variances and forecast final project costs.

What are the common challenges of project cost management?

The common challenges of project cost management are: inaccurate cost estimation, scope creep, inadequate expense monitoring, resource constraints, reporting delays, and lack of integration across teams.

Here, explaining these common challenges of project management:

1. Inaccurate cost estimation

Undermines the reliability of the entire budget before the project even begins. Estimating project costs is a complex process involving numerous assumptions, variables, and dependencies.

Account for scope, resources, quality standards, risks, and contingencies to avoid project constraints.

When these variables are misjudged due to insufficient data, limited experience, or incomplete scope analysis, the budget is flawed from day one, leaving the entire project financially vulnerable before a single task is completed.

2. Scope creep

Silently inflates costs and stretches timelines without formal financial accountability. As projects progress, stakeholders often request additions that fall outside the original scope.

When these requests move forward without proper approvals or change control, they quietly inflate costs and stretch timelines.

Even minor additions accumulate quickly, and without a formal process to evaluate their financial impact, budgets spiral before the team recognizes what has happened.

3. Inadequate expense monitoring

Allows budget issues to go undetected until they become costly and difficult to reverse. Without reliable systems to track project spending consistently, budget issues go undetected until they become serious problems.

Sporadic tracking or manual processes make it difficult to catch overruns in real time. By the time a cost issue surfaces, corrective action is either too late or far more expensive than it would have been had it been identified earlier.

4. Resource constraints

Resource limitations forces costly compromises when project demand exceeds what the budget can realistically support.

A limited budget restricts a project manager’s ability to secure and allocate the resources a project genuinely needs.

When resource availability does not align with project demand, whether that involves people, tools, or time, teams are forced into compromises that carry hidden costs.

Understaffing leads to delays, and delays almost always lead to budget overruns.

5. Reporting delays

Create a financial blind spot that turns manageable overruns into full-blown budget crises.

The gap between when costs are incurred and when they are reported seriously undermines financial decision-making.

When cost data is not captured and surfaced promptly, you work from outdated information.

What starts as a manageable overspend can quietly grow into a crisis before anyone has an accurate picture of the situation.

6. Lack of integration across teams

Fragments cost data across departments, eliminating any single source of financial truth.

When cost-related information is spread across finance, operations, and project teams without a shared system, the result is fragmented data, inconsistent reporting, and conflicting figures.

There is no single source of truth, making it nearly impossible to get an accurate, real-time view of where the budget actually stands.

Decisions made on siloed data are, at best, incomplete, and at worst, dangerously misleading.

What are the best tools and software for project cost management?

We have organized the best tools and software for project cost management into 4 categories: project management platforms, time tracking & budgeting tools, accounting & financial software, and enterprise cost management solutions.

Having the right tools in place determines how effectively you plan, track, and control costs in practice. Let’s learn more about these categories below:

1. Project management platforms

These platforms form the operational backbone of cost management, connecting task planning, resource allocation, and budget tracking in one place.

They give project managers a centralized view of what’s being worked on, by whom, and at what cost, making it easier to spot financial risks before they escalate.

For teams juggling multiple projects simultaneously, a strong project management platform is often the single most impactful investment for keeping costs under control. Sharing a few tools with you:

- ProofHub: An all-in-one project management platform that brings task tracking, time logging, and team collaboration into a single workspace. The tool is best for reducing the overhead costs that come with managing multiple disconnected tools.

- Monday.com: Offers a customizable platform with budget tracking by project phase, expense visualization, and alert notifications when spending deviates from the plan.

- Smartsheet: Provides budget templates broken down by phase or department, real-time burn charts, and financial governance controls suited for teams that prefer a structured, spreadsheet-style approach.

2. Time tracking and budgeting tools

When labor is a significant cost driver, these tools help teams understand exactly where hours and money are going.

These tools translate time logged on tasks directly into cost data, giving project managers an accurate picture of labor spend against the budget.

Without this visibility, labor costs, often the largest line item in a project budget, remain largely invisible until it’s too late to act.

- Toggl: Offers time tracking with built-in budget reporting, letting managers set hourly cost estimates per project and monitor labor spend as work happens.

- Harvest: It combines time tracking, expense logging, and invoicing in one tool, with direct integrations into accounting software like QuickBooks and Xero.

3. Accounting and financial software

Accounting & financial software tools handle the financial reporting side of cost management, ensuring project spend is accurately recorded and reconciled.

They sit at the intersection of project execution and business finance, translating project activity into the ledger entries, reports, and cash flow statements that leadership and stakeholders rely on.

For organizations managing client-facing projects, they also streamline invoicing and ensure billing stays aligned with actual project costs.

- QuickBooks: Is widely used for tracking project expenses, managing invoices, and generating financial reports, and integrates with most project management platforms.

- Xero: Offers cloud-based accounting with real-time visibility into cash flow, expenses, and project profitability, well-suited for small to mid-sized teams.

4. Enterprise cost management solutions

For large-scale or complex projects, these platforms provide financial control that goes beyond what general project management tools offer.

They are built to handle the scale, regulatory requirements, and multi-stakeholder complexity that enterprise projects demand.

They also support advanced capabilities like earned value management, multi-currency budgeting, and cross-departmental financial consolidation.

Organizations running large infrastructure, engineering, or ERP-integrated projects typically rely on these platforms as their system of record for cost performance.

- Oracle Primavera: Supports detailed cost planning, earned value management, and multi-project portfolio tracking, widely used in construction and infrastructure.

- SAP Project System: Integrates cost management directly into enterprise resource planning, giving large organizations a unified view of budgets, procurement, and financial reporting across departments.

Project cost management template

This project cost management template will help you plan, estimate, and control project expenses in a structured way. The template provides clear visibility into budgets, ensuring resources are allocated efficiently.

By tracking costs against the plan, it helps prevent overruns and supports better financial decision-making throughout the project lifecycle.

Get the free project cost management template

Download the free ProofHub Project Cost Management Template to simplify budgeting, track expenses with precision, and keep your project financially on track from start to finish.

Download templateHow to use this project cost management template

This template is designed to help you plan, track, and control your project costs in one place. Here is how to get started:

Step 1: Fill in the project information. Start by entering your project name, manager, client, and timeline at the top. This keeps the template tied to a specific project.

Step 2: Add your tasks and estimate costs. In the Cost Estimation & Tracking section, list your work packages, assign a resource type, and enter estimated hours and an hourly rate. The budgeted cost is calculated automatically.

Step 3: Log actual costs as work progresses. As the project moves forward, fill in the Actual Cost column for each task. The variance column updates automatically to show where you are over or under budget.

Step 4: Track your contingency reserve. Whenever an unplanned expense arises, log it in the Contingency Reserve section. The running balance updates automatically so you always know how much reserve is left.

Step 5: Review the variance summary at project close. The Cost Variance Summary gives you a category-level view of budgeted vs actual spend, helping you identify where estimates were off and improve planning for future projects.

Real-world example of project cost management

A mid-sized digital marketing agency decides to build a client portal — a simple web platform where clients can log in, view campaign reports, and download invoices.

The project manager is given a fixed budget of $18,000, a three-month deadline, and a small team of two developers, one designer, and one QA tester. Here is how cost management plays out.

Phase 1: The initial estimate overshoots the budget

When the project manager breaks the project down task by task, the estimate comes in at $19,500-$1,500 over budget.

After reviewing the scope with the team, they decide to remove a live chat feature and schedule it for a later update. The revised estimate comes down to $16,500.

A contingency reserve of $1,500 is added, bringing the total approved budget to $18,000. This becomes the cost baseline.

Phase 2: An early warning during development

Four weeks in, the project manager reviews spending and notices that the design phase has used $3,800 out of its $4,000 budget, but only 60% of the design work is done.

The designer had been making frequent revisions due to unclear client feedback, which was eating up hours without producing finished work.

The project manager steps in, sets up a structured feedback process with the client, and caps further revisions to two rounds. This brings the design phase back on track without any additional cost.

Phase 3: An unexpected third-party tool cost

In month two, the team realizes they need a third-party plugin for generating PDF invoices inside the portal.

It costs $600, which was not included in the original estimate.

Rather than ignoring it, the project manager logs it as an unplanned expense and covers it from the contingency reserve. The rest of the budget remains untouched.

Phase 4: Project delivered on budget

The portal goes live at the end of month three. Total spend comes in at $17,200-$800 under the cost baseline, with $900 of the contingency reserve still remaining.

At the project close review, the team notes two things: client feedback loops need to be defined before design begins, and third-party tool requirements should be researched during the estimation phase.

Both are added to the agency’s project checklist for future builds.

How to prevent and control cost overruns?

To prevent and control cost overruns, define the scope clearly before estimating costs. Use realistic estimation techniques, set a contingency reserve, track costs frequently, not just at milestones, control scope creep with a formal change process, and act on warning signs immediately.

Here are the details of these pointers to prevent and control cost overruns:

- Define the scope clearly before estimating costs. Most overruns start with an incomplete scope. When deliverables are not clearly defined upfront, estimates are built on assumptions that fall apart during execution.

- Use realistic estimation techniques. Optimistic guessing is one of the biggest budget killers. Using structured approaches like bottom-up or three-point estimating produces numbers grounded in actual project requirements rather than best-case thinking.

- Set a contingency reserve. Unexpected costs are not a matter of if; they are a matter of when. Setting aside 10–15% of the total budget gives the project a financial buffer without derailing the baseline.

- Track costs frequently, not just at milestones. Waiting until a milestone review to check spending means overruns have already been building for weeks. Weekly cost reviews allow project managers to catch variances early when they are still manageable.

- Control scope creep with a formal change process. Every unreviewed addition to the project scope carries a hidden cost. A formal change request process ensures no new work begins without assessing its financial impact first.

- Act on warning signs immediately. A cost variance spotted at week three is a small problem. The same variance ignored until week eight is a crisis. Early visibility only creates value when it is followed by early action.

What are common cost overruns in projects?

The common cost overruns in projects are: poor scope definition, inaccurate cost estimation, uncontrolled scope creep, resource mismanagement, schedule delays, and unexpected external factors.

Here are the explanations:

- Poor scope definition: When the project scope is not clearly defined from the start, teams end up discovering new requirements mid-execution. Each undocumented requirement adds work, time, and cost that was never accounted for in the original budget.

- Inaccurate cost estimation: Underestimating the cost of tasks, whether due to limited experience, missing data, or overly optimistic assumptions, sets the project up for a budget shortfall before work even begins. The further the estimate is from reality, the harder it becomes to recover.

- Uncontrolled scope creep: Small additions requested by stakeholders or clients may seem harmless in isolation, but without a formal approval process, they accumulate quickly. What starts as a minor feature request often ends up consuming a significant portion of the remaining budget.

- Resource mismanagement: Assigning the wrong people to tasks, overloading team members, or failing to plan for resource availability leads to inefficiencies that cost money. Idle time, rework, and last-minute hiring are all direct consequences of poor resource planning.

- Schedule delays: Time and cost are directly linked in most projects. When timelines slip due to dependencies, bottlenecks, or poor planning, the cost of keeping the team engaged beyond the original deadline adds up fast.

- Unexpected external factors: Vendor price increases, supply chain disruptions, regulatory changes, or sudden team turnover can all introduce costs that no estimate could have fully anticipated. Without a contingency reserve, these events hit the budget with full force.

How does cost management relate to the triple constraint?

Cost management relates to the triple constraint by being one of its three core boundaries: scope, time, and cost, which together define the boundaries of every project.

These three elements are interdependent, meaning a change in any one of them will almost always affect the other two.

Think of it as a triangle. When scope expands, costs go up, and timelines stretch. When the deadline is pushed forward, either costs increase to bring in more resources or scope has to be reduced.

When the budget is cut, the team must either deliver less or take longer. No side of the triangle can shift without the others responding.

What is the difference between cost management and project budget?

The difference between cost management and project budget is that cost management is the ongoing process of planning, estimating, monitoring, and controlling expenses throughout the entire project lifecycle.

It is not a one-time activity; it is a continuous discipline that ensures the project stays financially on track from start to finish.

The project budget is the approved financial plan that defines how much money is allocated to complete the project. It is a fixed document established during the planning phase that serves as the baseline against which all actual spending is measured.

| Basis | Cost Management | Project Budget |

| Definition | Process of planning, tracking, and controlling project costs | Approved financial plan allocating funds to the project |

| Nature | Ongoing and dynamic | Fixed and established upfront |

| Purpose | Ensures spending stays within approved limits | Sets the financial boundaries for the project |

| Scope | Covers the entire project lifecycle | Created during the planning phase |

| Flexibility | Adapts as project conditions change | Changes only through formal approval |

| Focus | Actions and decisions around spending | Numbers and financial allocations |

| Outcome | Controlled and predictable project finances | A baseline to measure actual spend against |

Is cost management required in Agile projects?

Yes, cost management is required in Agile projects, but it works differently than in traditional project management.

Agile teams operate on a fixed budget with a flexible scope, meaning cost management shifts from tracking individual task estimates to monitoring the cost of ongoing delivery sprint by sprint.

Every backlog prioritization decision is also a cost decision: what gets built, what gets deferred, and what gets dropped all directly affect how the budget is consumed.

What is the impact of AI on project cost forecasting accuracy?

AI significantly improves project cost forecasting accuracy by analyzing large volumes of historical project data, identifying spending patterns, and flagging potential cost risks before they materialize.

Unlike manual forecasting, AI-powered tools can process real-time cost data and continuously update projections as project conditions change.

This reduces reliance on human estimation, which is often optimistic or incomplete, and gives project managers earlier, more reliable signals to make informed budget decisions.